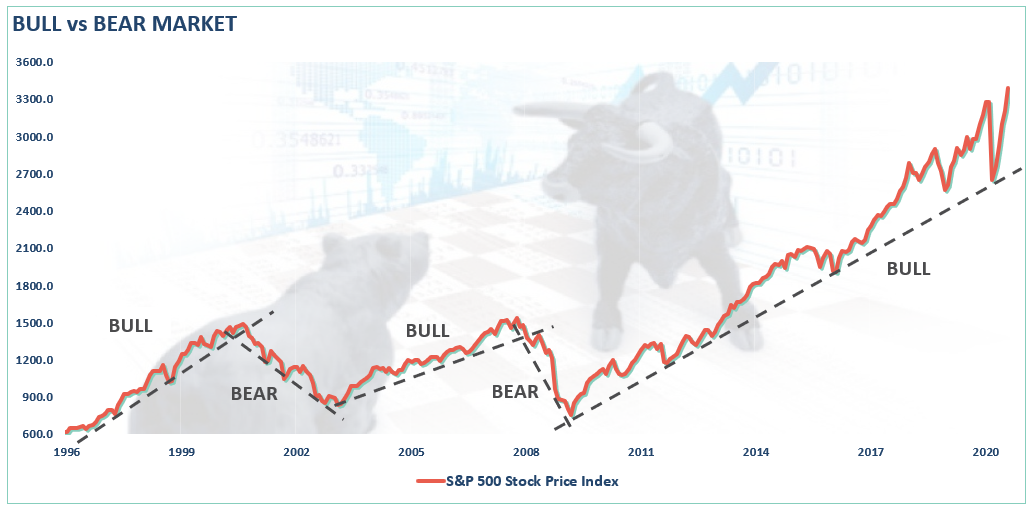

1. Is it time to take some profits on your appreciated stocks? Do need to explore the world of option collars to protect your gains? Is it time for another stock market correction? The Federal Reserve and Treasury Department have other ideas but history says one is eventually coming. All stock markets are cyclical. They follow the business cycle, which, of course, is also cyclical. But government stimulus has prolonged both the business cycle and the stock market. If you look at the Nasdaq's recent gain your conclusion might be this bull market is not done and that the US will overcome the recent drop in GDP and increase in unemployment and power the economy from one cycle high to the next one without much of a bump.

We have now concluded 12 years of this historic bull market which began in March of 2009, It is greater in longevity than the three prior biggest bull markets in US history. The US stock market has never gone up more than 11 years in a row but then again, it had never went up more than 8 years in a row as it continues to set longevity records. With continued Federal Reserve and Treasury stimulus, this bull market continues to ignore the skeptics and power forward.

The following chart estimates the future returns of the stock market at its current peak. It is based on fundamentals such as the level of corporate earnings today compared to their stock price. Based on past history, stock prices are way ahead of their current and estimated earnings. Ten year future returns look flat. We are at the 1929 level of over valuation. The market from that point took 25 years to 1955 to recover to the peak level reached in 1929. It took 16 years for the market to recover from 1966 to 1982. This does not mean the stock market cannot continue to advance. With stimulus provided by massive deficit spending by the Treasury and the continued printing money out of thin air (QE) by the Federal Reserve, the market can continue upward. It has continued to confound the fundamental experts and has kept plowing forward. But counting on high future returns from this level without at least considering taking some well deserved profits through by collaring might be pushing one's luck.

"Given any set of future cash flows, the higher the price you pay today, the lower the long-term rate of return you can expect on your investment. Nothing about this relies on mean-reversion. It’s just arithmetic. For any given set of expected future cash flows, knowing the price immediately tells you the expected return. Knowing the expected return immediately tells you the price. It’s just arithmetic. You don’t need to “adjust” these calculations for the level of interest rates. Now, once you calculate the expected investment return, you can certainly compare it with the level of interest rates, but the idea that valuations have to be “corrected” for interest rates reflects a misunderstanding of basic finance." (Hussman)

2. “Defensive Sectors Are Not Much Help In Market Downturns! Sy Harding May 9, 2014.

Wall Street’s advice on how to prepare for possible market corrections has always been the same. No matter what happens to the economy people will still have to eat, drink, and take their medicines. So consumer staples, food, beverage, healthcare, and drug companies will do well even in economic and market downturns. Also on the list are large solid companies with stable earnings, particularly those like utilities that pay solid dividends that should offset declines in their stock prices.

As one prominent brokerage firm posts on its website, “Defensive stocks represent necessary items, like food, gas and medicine, and tend to change very little with the economic cycle because consumers are likely to continue buying them even in tough economic times.”

Defensive stocks currently recommended by Wall Street firms include the usual; Proctor & Gamble (PG), Kellogg (K), Coca Cola (KO), PepsiCo (PEP), WalMart (WMT), McDonald’s (MCD), Johnson & Johnson (JNJ), Amgen (AMGN), Pfizer (PFE), and utilities companies.

However, investors need to be aware that while consumers will indeed have to continue to eat, drink, and take their medicines, and therefore continue to buy the products of those companies, in a market decline investors do not have to continue to value the earnings of those companies as highly as during an exciting bull market. Furthermore, they do not.

In the enthusiasm of a bull market investors may be willing to pay 20 times earnings for a stock, while in the throes of a serious market decline they will perhaps pay only 12 times earnings for the same stock. Thus, although a company’s earnings may continue to grow, even ‘defensive’ sector companies see their stocks decline in value in a market correction.

For instance, in the 2000-2002 bear market, the recommended ‘defensive’ stocks included Alcoa, Bristol Myer Squibb, Citigroup, Coca-Cola, Disney, DuPont, Fannie Mae, General Electric, Home Depot, IBM, Merck, and WalMart. They plunged an average of 59% to their lows, worse than the Dow’s decline of 38% and the S&P 500 decline of 49%.

The utility sector was also highly recommended as portfolio protection, since utilities are noted for paying high dividends. However, the DJ Utilities Average plunged 60% in the 2000-2002 bear market, more than the S&P 500’s 49% decline.

In the 2007-2009 bear market, using ETFs as a proxy for the ‘defensive’ sectors, while the S&P 500 lost 50% of its value, the HLDRS Pharmaceuticals ETF (PPH) declined 43%, the Van Guard Healthcare ETF (VHT) plunged 42%, and the SPDR Consumer Staples ETF (XLP), fell 35%. Meanwhile, the dividend-paying DJ Utilities Index plunged 48%.

Those were severe bear markets. How do ‘defensive’ sectors perform in less severe 10% to 15% corrections? Let’s look at their performance in the last one, the summer correction in 2011.

The Dow declined 16% in that correction. The VanGuard Healthcare ETF (VHT) declined 17%. The HLDRS Pharmaceuticals ETF (PPH) declined 14%. The SPDR Consumer Staples ETF (XLP) fell 10%. Meanwhile, the DJ Utilities Avg. declined 13%.

History seems to show that re-positioning a portfolio into so-called defensive sector holdings when risk rises of a market correction does not provide much, if any, protection.

Is there a better approach? Moving to higher cash levels to avoid losses would seem to be one. (I would add a put option strategy or an option collar). Keep in mind that a $100,000 portfolio that loses 50% of its value to $50,000, then needs a 100% gain to get back to even.

Currently, it’s not surprising that with rising concerns of a possible correction this fall, investors have been piling into the touted ‘defensive’ sectors to such a degree that they are outperforming the market so far this year. As long as the market holds up they may be better than average holdings. However, history shows that investors preparing for a potential correction by piling into ‘defensive’ sectors, on the expectation that they will protect portfolios in downturns, are likely to be disappointed, to say the least.”